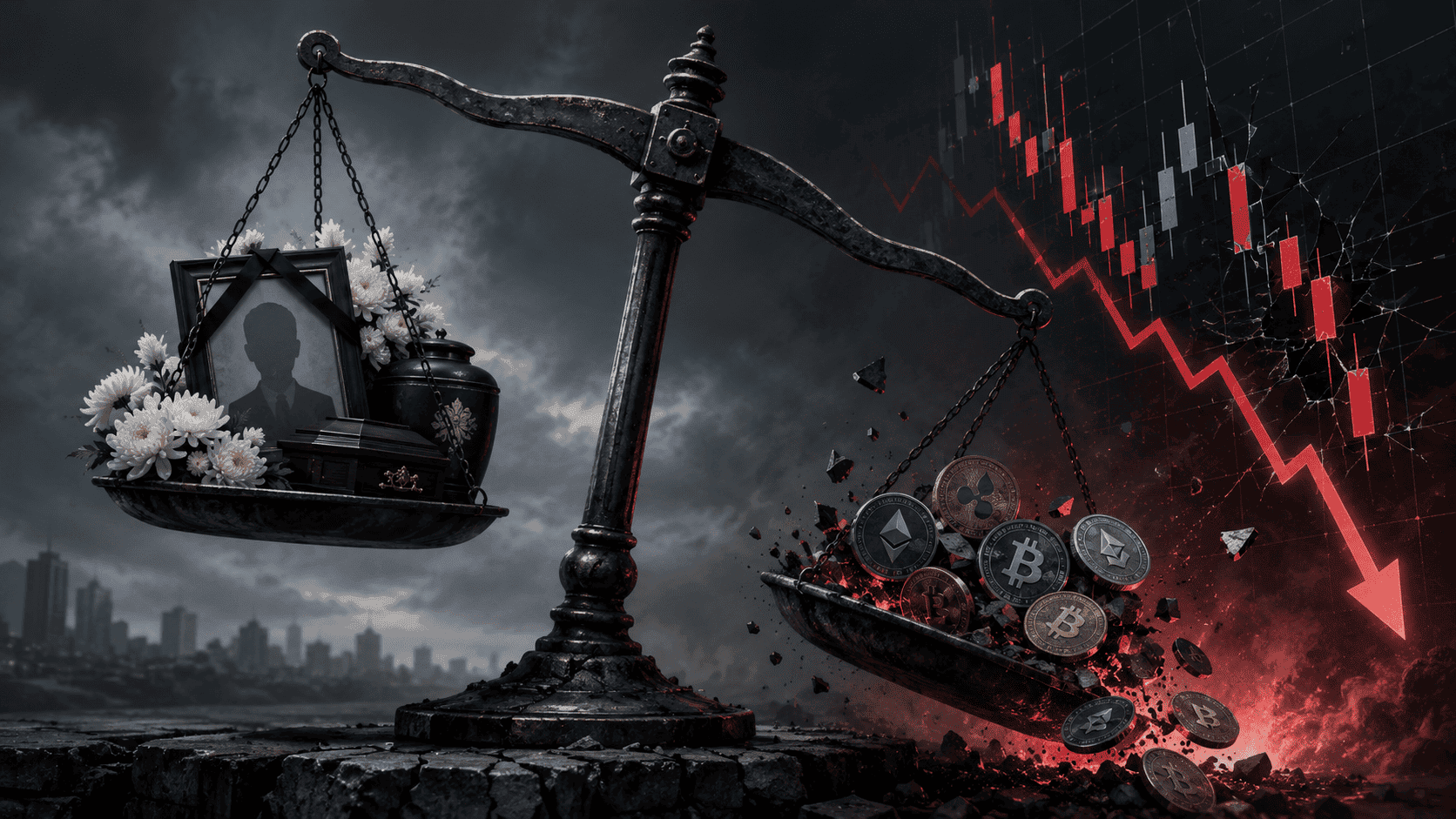

Bumo Sarang, one of South Korea’s largest funeral service providers, secretly invested approximately $40 million of its customers’ prepaid funeral deposits into a leveraged cryptocurrency ETF. By the end of 2025, that investment had lost over $33 million, leaving the company with just $6.8 million from an original $40 million position.

The company’s name translates to “Parent’s Love.” Its customers are everyday South Koreans who pay monthly instalments to lock in the cost of future funeral services for their parents and family members. These are some of the most conservative financial consumers imaginable, people planning ahead for one of life’s most difficult moments.

Their money ended up in a 2x leveraged ETF that bets on the daily price swings of an Ethereum treasury company. Nobody told them.

How a Funeral Firm Ended Up in Leveraged Crypto

The mechanics of how this happened reveal a regulatory gap that goes far beyond one company.

South Korea’s funeral mutual aid industry works on a prepayment model. Customers pay small monthly amounts over many years, building up a pool of capital that the company is supposed to hold safely until services are needed. It’s similar to an insurance product, except with far less oversight.

Under current South Korean law, funeral service providers are only required to keep 50% of customer prepayments in safe, conservative investments. The other half can be invested in virtually anything, including leveraged derivatives. That’s because these companies are regulated by the Fair Trade Commission as “prepaid instalment operators,” not by financial regulators as actual financial institutions.

Bumo Sarang used that freedom to make a massive bet. The company put $40 million into the T-REX 2X Long BMNR Daily Target ETF (ticker: BMNU), a US-listed product designed to deliver twice the daily return of Bitmine Immersion Technologies. Bitmine is the world’s largest corporate holder of Ethereum, with roughly 5.2 million ETH worth about $12.3 billion on its balance sheet.

In simple terms, Bumo Sarang was making a double-leveraged bet on a company whose value rises and falls with Ethereum’s price. When the crypto market declined throughout late 2025 and into 2026, the ETF’s value collapsed. The $40 million investment shrank to $6.8 million.

Leveraged ETFs Are Not Built for Long-Term Holding

This is a critical detail that many people outside of professional trading don’t understand. Leveraged ETFs are designed for day trading. They are explicitly not intended to be held over weeks or months, let alone an entire year.

The reason is something called “volatility decay.” A 2x leveraged ETF resets its exposure every single day. If the underlying asset goes up 10% one day and down 10% the next, you don’t end up back where you started. You end up with less. Over time, this daily reset erodes the value of the fund even if the underlying asset stays roughly flat.

When the underlying asset actually declines significantly, as Ethereum did during the period Bumo Sarang held the ETF, the losses are amplified dramatically. A 50% decline in the underlying asset can translate into a near-total loss in a 2x leveraged product over the same period.

Bumo Sarang described its position as a “short-term unrealized loss” caused by market instability. But holding a daily-reset leveraged ETF for an entire year is the opposite of a short-term trade. It suggests either a fundamental misunderstanding of the product, or a calculated gamble that went badly wrong.

Either way, the people paying the price are customers who signed up for funeral services, not for exposure to leveraged crypto derivatives.

This Is Not an Isolated Case

The most disturbing part of this story is that Bumo Sarang is just the most visible example of a much wider problem.

An investigation by Korea Economic Daily examined 75 funeral mutual aid companies and found that 32 of them, roughly 43%, held fewer assets than they owed to customers. In plain terms, nearly half of these companies are technically insolvent. If all their customers asked for refunds at once, they wouldn’t have the money to pay them back.

The investigation also flagged a pattern of related-party lending, where some funeral companies issued loans to their own major shareholders in amounts that exceeded total customer payments. That’s not investment mismanagement. That’s closer to the kind of self-dealing that brought down FTX.

The funeral mutual aid market in South Korea is estimated at around 10 trillion won (roughly $7 billion). It serves millions of customers who have limited visibility into how their money is being managed. And until now, the regulatory framework hasn’t required much transparency or imposed meaningful restrictions on investment activity.

South Korea Is Scrambling to Fix the Problem

The fallout has been swift. As of May 2026, six legislative proposals are working their way through the Korean parliament. The proposed reforms would restrict the types of investments funeral companies can make with customer funds and ban loans to major shareholders entirely.

The Fair Trade Commission is also increasing scrutiny of the industry, requiring more detailed financial disclosures and more frequent audits. The goal is to close the regulatory gap that allowed a funeral company to bet customer deposits on leveraged crypto products without anyone noticing until the money was already gone.

Whether these reforms come fast enough to protect current customers is an open question. The 32 companies identified as having insufficient assets to cover customer obligations represent millions of people whose prepaid funeral plans may not be fully backed.

For the crypto industry specifically, this story adds another data point to the ongoing debate about leveraged products and investor protection. South Korea is already preparing to impose a 22% crypto tax in January 2027. Incidents like this strengthen the hand of regulators who argue that the crypto space needs tighter controls, even when the actual problem is a lack of financial regulation in a completely unrelated industry.

The Lesson for Every Crypto Investor

Bumo Sarang’s story is extreme, but the underlying mistake is one that regular investors make all the time: using a financial product without understanding how it works.

Leveraged ETFs are powerful tools in the right hands. Professional day traders use them to amplify short-term moves. But they are designed to be held for hours or days, not months. Holding them over longer periods almost always results in underperformance relative to the underlying asset, and in a declining market, the losses can be devastating.

The broader lesson is about due diligence. Whether you’re a company investing customer funds or an individual managing your own portfolio, understanding the products you’re putting money into is not optional. The people who lost $33 million weren’t sophisticated crypto traders. They were a funeral company that apparently didn’t understand what a 2x leveraged daily-reset ETF actually does over time.

If a product promises to double your returns, it can also more than double your losses. That’s not a crypto problem. That’s a leverage problem. And it’s a lesson the industry keeps learning the hard way.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments carry significant risk. Always conduct your own research before making any investment decisions.