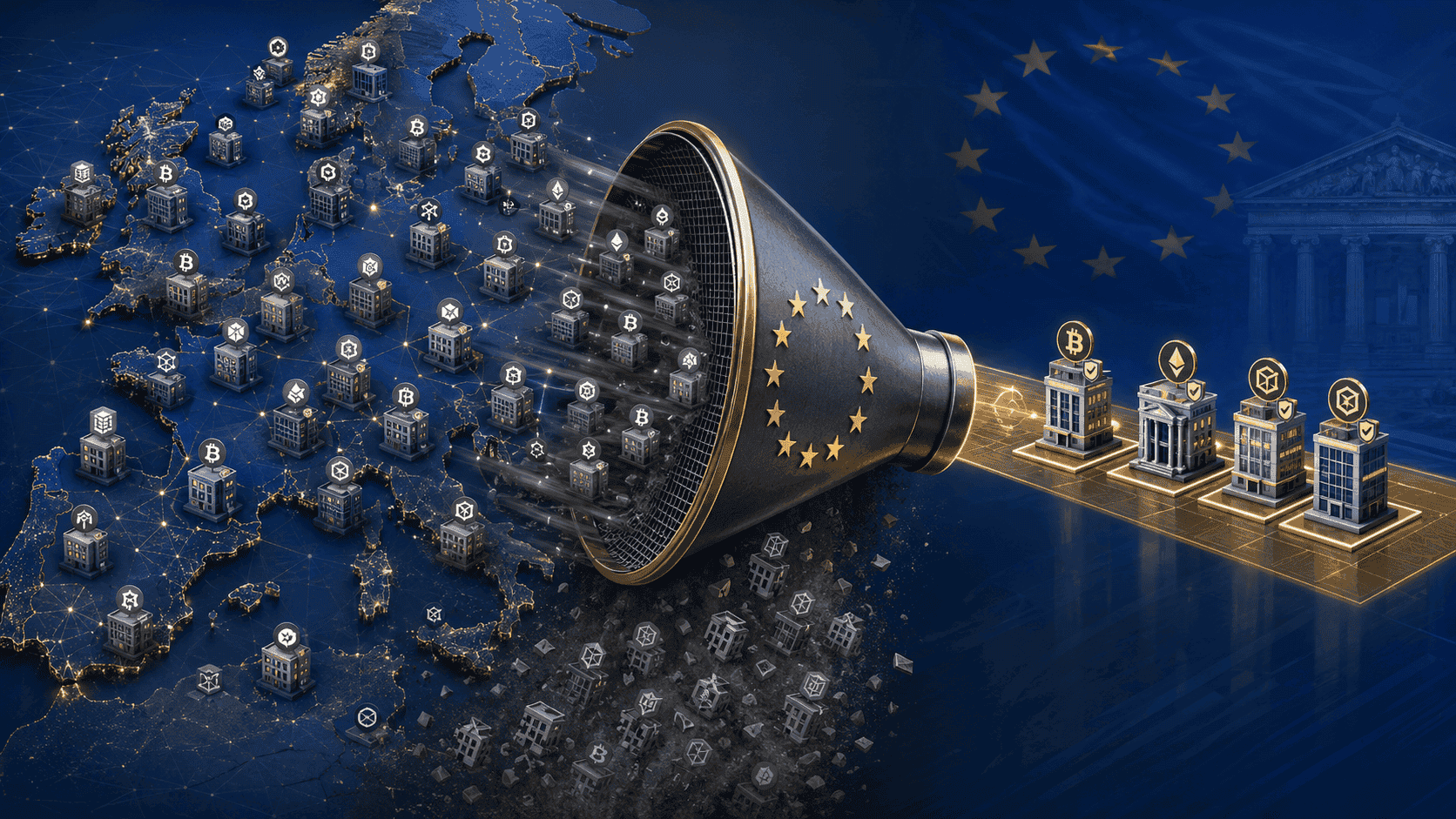

On July 1, 2026, the European Union’s grandfathering transition window under the Markets in Crypto-Assets regulation officially ends. After that date, any crypto exchange, broker, or wallet provider without a valid MiCA license must stop serving EU customers immediately. The European Securities and Markets Authority has been explicit: there will be no further grace periods, no extensions, no exceptions.

The numbers explaining what this means are stark. According to legal analysis by Hogan Lovells, Europe had more than 3,000 registered virtual asset service providers in 2024. As of May 2026, only 194 firms had secured MiCA authorization across the EU, including credit institutions. Hogan Lovells estimates that approximately 75% of pre-MiCA providers will lose their registration status when the deadline hits.

For context: Poland alone accounted for more than 1,400 legacy registrations under the pre-MiCA system. France’s market regulator has warned that non-compliant operators face criminal penalties including fines and up to two years in prison. Italy, Germany, the Netherlands, and Spain all maintain similar enforcement stances. The framework is the strictest, most coordinated crypto regulation any major economic bloc has ever implemented at scale.

This is no longer hypothetical regulatory pressure. It’s a structural reset of the European crypto industry happening in 16 days. For users on platforms that won’t make the cut, withdrawal deadlines are approaching. For firms scrambling to obtain authorisation, the window is closing. For the broader crypto industry, the European market is about to look fundamentally different than it does today.

The 3,000 to 194 Gap

The disparity between registered providers in 2024 and authorised providers in 2026 reflects the brutal selectivity of MiCA’s licensing process.

Pre-MiCA, individual EU member states maintained their own registration regimes for crypto firms. Some, particularly Poland, Estonia, and Lithuania, had relatively light-touch requirements that allowed hundreds of small operators to register without extensive compliance infrastructure. Other countries including Germany and France maintained stricter standards. The result was a fragmented patchwork where the same firm could face wildly different requirements depending on which member state it operated from.

MiCA harmonised the requirements across all 27 EU member states. The standardised framework is significantly more demanding than the average pre-MiCA regime. It requires substantial capital reserves, comprehensive compliance programmes, detailed governance documentation, robust risk management frameworks, and ongoing reporting obligations. For small firms operating with minimal infrastructure, the compliance cost alone can be prohibitive.

The 75% figure that Hogan Lovells projects isn’t a worst-case scenario. It’s the law firm’s central estimate based on the gap between firms that registered pre-MiCA and firms that have either obtained or are reasonably positioned to obtain MiCA authorisation. Many of those 3,000+ legacy firms were small operators that registered to take advantage of permissive jurisdictions like Poland but never built the operational infrastructure that MiCA requires.

The remaining 194 authorised firms include the major exchanges and infrastructure providers that have been preparing for MiCA since the regulation was finalised in 2023. Binance, Coinbase, Kraken, Bitstamp, and other large international platforms have either secured authorisation or are well advanced in the application process. The biggest losers from July 1 will be smaller regional operators that lacked the resources to navigate the new framework.

What Happens on July 1

ESMA’s guidance for the transition is specific and unforgiving. Crypto firms operating without MiCA authorisation after July 1 will be in breach of EU law and must immediately cease providing crypto-asset services to EU clients.

The cessation isn’t optional or gradual. Firms expected to fall under the deadline must stop accepting new deposits immediately. They must help existing customers withdraw assets, transfer funds to authorised providers, or move to self-hosted wallets. ESMA’s guidance explicitly states that firms are expected to have “orderly wind-down plans” in place if they cannot obtain authorisation in time.

For users, the implications are significant. Accounts on non-authorised platforms will become inaccessible for new transactions. Withdrawal windows may close. Account verification may be required to facilitate the transfer of assets to compliant providers. The administrative burden of moving funds, reverifying identity, and adapting to new platforms will fall on millions of European crypto users.

The most affected users will be those on smaller regional platforms that historically offered lower fees, more product variety, or better local support than the major international exchanges. Those users will face a forced migration to larger platforms that may not match their preferences, or they may need to consider self-custody solutions that require greater technical knowledge.

Enforcement will be coordinated across all 27 EU member states through national regulators. France’s AMF has indicated it will pursue criminal penalties for continuing operations without authorisation. Germany’s BaFin maintains similar enforcement stances. The cross-border coordination means there will be no jurisdiction within the EU where unlicensed operations can continue without legal consequence.

The Regional Variations That Matter

Not every EU member state is equally prepared for the transition. Poland presents the most acute case. The country was among the most popular pre-MiCA jurisdictions due to its permissive registration regime, accounting for more than 1,400 legacy providers. As of March 2026, Poland’s local MiCA implementation legislation had still not passed, leaving Polish providers in a state of regulatory uncertainty that complicates their transition planning.

France presents a different kind of warning. As of January 2026, only 30% of roughly 90 unlicensed French firms had applied for MiCA authorisation. A further 40% indicated they did not intend to apply at all. The French data suggests that a significant percentage of providers have effectively decided to exit the EU market rather than pursue authorisation, accepting the loss of their European customer base.

Germany, the Netherlands, and Spain have been more aggressive in pushing firms toward compliance. Their licensing authorities have provided clearer guidance and faster processing times, resulting in higher proportions of regional providers either obtaining authorisation or initiating credible applications. Firms based in these jurisdictions have generally been better positioned for the transition.

Italy’s regulatory framework has historically been complex, and Italian providers face significant uncertainty about how local enforcement will proceed. Smaller member states including Lithuania, Estonia, and Malta have varying preparation levels. The patchwork of national readiness will produce uneven enforcement across the EU, particularly in the first months following July 1.

For users, the implication is that the platform they use matters even more than usual. Two firms operating similar businesses can have very different MiCA outcomes depending on which member state they’re domiciled in and how that member state’s regulator is processing applications.

The Broader Implications for Crypto

MiCA’s hard deadline represents the most significant regulatory consolidation event in crypto’s history. The implications extend beyond European borders.

For the surviving 194 authorised providers, MiCA creates a meaningful competitive moat. Operating across the EU under a single license, while competitors are forced to either obtain similar licenses or exit, provides authorised firms with access to a unified market of approximately 450 million people. The licensing investment, expensive and time-consuming, transforms into a long-term competitive advantage as smaller competitors are forced out.

For users, the consolidation produces a smaller selection of compliant providers but potentially better consumer protections. MiCA requires firms to maintain customer fund segregation, hold appropriate capital reserves, and operate transparent compliance frameworks. The fewer compliant providers should theoretically offer higher service standards than the average pre-MiCA operator.

For the global crypto industry, MiCA serves as a template that other major economies are watching closely. The UK is developing its own crypto framework that draws on MiCA’s structure. The US has been negotiating the CLARITY Act, which addresses similar market structure questions through a different regulatory approach. Singapore, Hong Kong, and Dubai have all been developing licensing regimes that incorporate elements of MiCA’s framework. The European experience over the coming months will inform how other jurisdictions structure their own crypto regulations.

The risk that critics flag is regulatory capture and reduced competition. With approximately 75% of providers being eliminated by a single regulatory deadline, the surviving firms gain significant pricing power and reduced competitive pressure. Innovation that previously happened at smaller, more experimental firms may be channelled away from the European market. Some users may migrate to offshore platforms or decentralised venues that operate outside MiCA’s reach, potentially exposing themselves to higher risks than the regulated framework was designed to mitigate.

What Users Should Do

The practical advice for European crypto users with less than 16 days until the deadline is straightforward but urgent.

First, verify whether your current platform holds MiCA authorisation. ESMA maintains an Interim MiCA Register, last updated on June 12, that lists all authorised firms. The register is the official source for verification, and users should check it directly rather than relying on platform marketing claims.

Second, if your platform is not authorised, plan a withdrawal or migration before the deadline. Withdrawing crypto to a self-hosted wallet provides full control but requires technical knowledge and careful security practices. Migrating to an authorised platform is simpler but requires opening a new account, completing identity verification, and transferring funds.

Third, be cautious of fraud attempts that will inevitably exploit the transition. Scammers will likely send fake notices claiming to require account updates, identity verification, or wallet transfers. Verify any communication directly through the platform’s official channels and never click suspicious links related to MiCA migration.

Fourth, consider that some platforms may continue operating even without authorisation, in violation of EU law. Using such platforms exposes users to legal complications and limited recourse if disputes arise. The short-term convenience of avoiding a migration is rarely worth the long-term risk of using a non-compliant provider.

For users with significant crypto holdings, consulting a tax or legal professional regarding the implications of forced migration may be worthwhile. The transition could trigger tax events depending on individual circumstances and jurisdiction-specific rules.

The European crypto industry is undergoing a regulatory transformation that will define its structure for years. The cleanup will be painful for affected providers and disruptive for affected users. The end result, ESMA argues, is a safer, more transparent, more consumer-friendly market. Whether that’s the actual outcome depends on how the next several months unfold.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Cryptocurrency investments carry significant risk. Always conduct your own research before making any investment decisions.