Behind every romance scam is a person who believed they had met someone real. A message that felt genuine. A relationship that grew over weeks or months. Then an investment opportunity, a crisis, a request for money. By the time the victim realizes the person never existed, their savings are gone, moved through a chain of cryptocurrency wallets designed to make the money impossible to trace.

Interpol just pulled back the curtain on how vast that machinery has become.

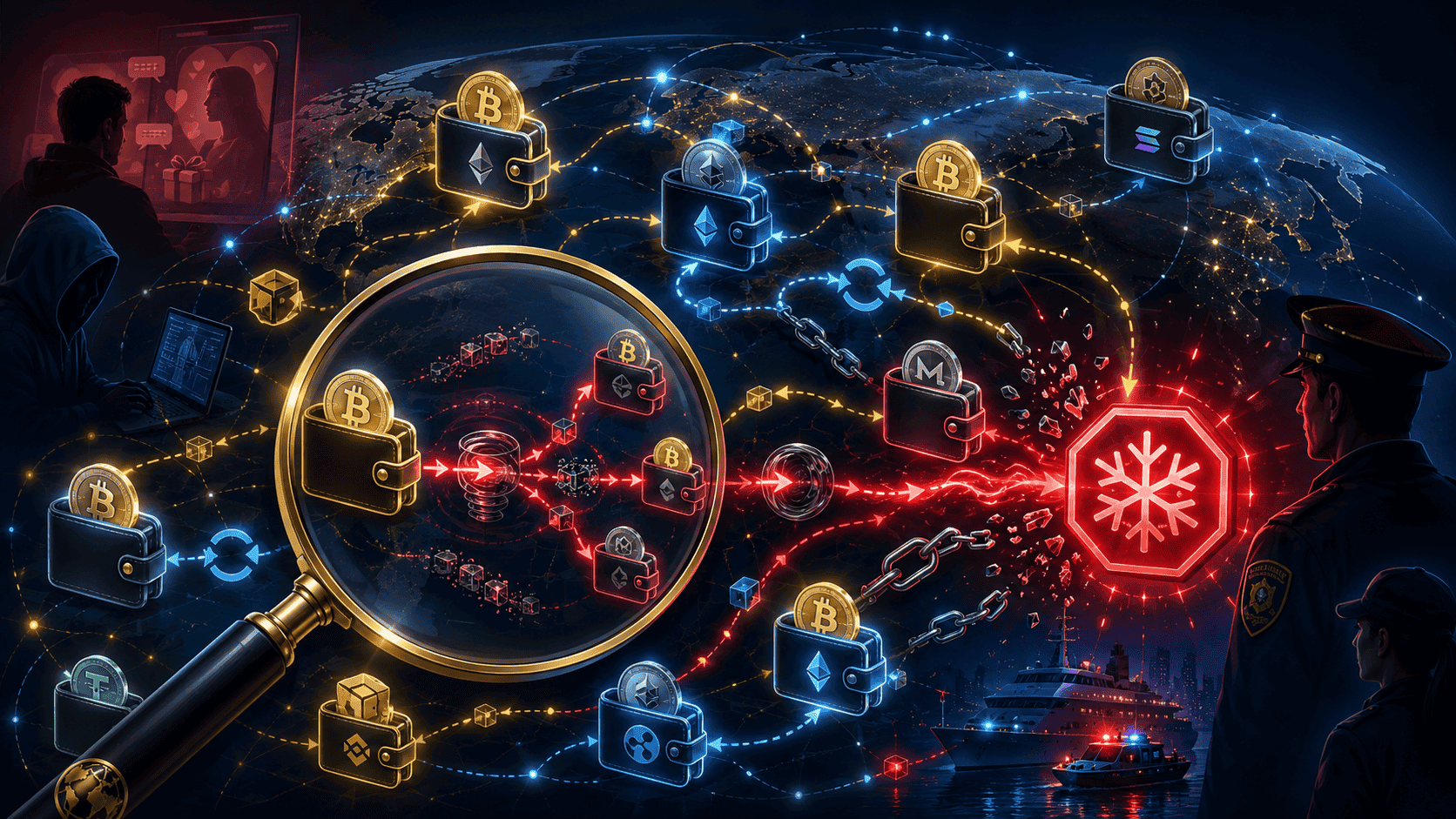

In a statement on July 9, Interpol revealed that a single cryptocurrency wallet controlled by a 20-year-old suspect in Thailand had processed more than $122.5 million in just 10 months. The money came from romance-scam victims around the world. The wallet was one node in a laundering network that used cross-chain token swaps, hopping funds between different cryptocurrencies, to obscure the financial trail and make the stolen money nearly impossible to follow.

The discovery came out of Operation First Light 2026, one of the largest coordinated anti-fraud campaigns Interpol has ever run. Spanning 97 countries and territories from January 15 to April 30, the operation resulted in 5,811 arrests and the interception of $293 million in illicit assets. More than 142,000 victims were identified. Over 31,000 bank accounts were frozen. It’s a staggering scale, and it still only scratches the surface of a criminal industry that United Nations investigators estimate generated tens of billions of dollars between 2020 and 2024.

How the Laundering Actually Works

The $122.5 million wallet illustrates a technique that has become the backbone of modern scam laundering: cross-chain swaps.

When scammers steal cryptocurrency from a victim, the funds start out traceable. Blockchain transactions are public, so investigators can theoretically follow the money. Cross-chain swapping breaks that trail. The launderers take stolen funds on one blockchain, swap them for a different cryptocurrency on another blockchain, then repeat the process across multiple chains and tokens. Each hop adds a layer of complexity, and because different blockchains don’t share a single ledger, following the money across all of them becomes extraordinarily difficult.

By the time the funds have bounced through several cryptocurrencies, the connection back to the original theft is buried under layers of transactions. The launderers can then cash out through exchanges, over-the-counter brokers, or other off-ramps with the origin of the money effectively hidden.

The scale that one 20-year-old’s wallet handled, over $122 million in under a year, reveals how industrialized this has become. This isn’t a lone scammer. It’s infrastructure. The individual controlling the wallet was likely a small cog in a much larger organized network, processing the proceeds of countless separate scams through a single laundering pipeline.

The romance scams feeding these wallets are themselves industrialized. Many operate from fortified compounds in Southeast Asia that, according to UN investigators, frequently rely on trafficked and coerced labor. People are lured with fake job offers, then forced to run scams under threat. The victims on both ends, the trafficked workers running the scams and the deceived people losing their savings, are casualties of the same criminal enterprise.

How Interpol Fought Back

The operation’s most important weapon wasn’t arrests. It was speed.

Interpol deployed its Global Rapid Intervention of Payments mechanism, known as I-GRIP, throughout the campaign. I-GRIP is a stop-payment system that lets authorities across different countries rapidly block or freeze suspicious transfers of both traditional currency and virtual assets before they settle and disappear. In the world of crypto fraud, where funds can be laundered and cashed out within hours, the ability to freeze money quickly is often the difference between recovering it and losing it forever.

The system proved its value repeatedly during the operation. Authorities in Singapore and Oman used I-GRIP to block a $6.6 million illicit transfer linked to a business email compromise scam, where criminals impersonated a supplier to a Singapore-based commodity trading firm. In Macao, police discovered during community outreach that a member of the public was being manipulated in real time by scammers posing as officials, and intervened before the victim could send nearly $372,000.

Some of the busts revealed the elaborate theater these criminals use. In Eswatini, police arrested 82 people and dismantled a network that had built a realistic replica of a Brazilian police station, complete with fake uniforms, signage, and equipment. The scammers ran video calls posing as Brazil’s Federal Police, convincing victims they were under investigation and persuading them to transfer funds for “safekeeping,” which then vanished.

The operation drew on a genuinely global coalition. It was coordinated by Interpol with funding from China’s Ministry of Public Security and support from regional policing bodies across Southeast Asia, the Gulf, and Europe. Tomonobu Kaya, director of Interpol’s Financial Crime and Anti-Corruption Centre, summed up the core lesson: criminal syndicates exploit human psychology to manipulate their targets, and no single nation can stay safe unless all countries fight back together.

Why This Matters for Crypto

The operation raises uncomfortable but important questions for the cryptocurrency industry, and it’s worth engaging with them honestly rather than defensively.

Crypto’s core features, fast settlement, global reach, and the ability to move value without traditional intermediaries, are genuine benefits for legitimate users. But those same features are exactly what make it attractive for laundering. The $122.5 million wallet worked because crypto let stolen funds move across borders and between assets faster than traditional systems could track them. Pretending this isn’t a real problem does the industry no favors.

At the same time, the operation demonstrates that crypto’s transparency is also a tool against crime. Because blockchain transactions are public and permanent, investigators could identify the wallet, trace its $122.5 million in activity, and build the case that led to arrests. Cash leaves no such trail. The same public ledgers that scammers try to obscure with cross-chain swaps ultimately give investigators a permanent record to analyze, and blockchain analytics have become increasingly sophisticated at untangling even complex laundering chains.

The trend line matters for regulation too. Operations like First Light strengthen the argument for the kind of anti-money-laundering rules being written into crypto legislation worldwide, from Europe’s MiCA framework to the licensing regimes emerging across Asia. The industry’s long-term legitimacy depends partly on its ability to prevent this kind of abuse, and cooperation between exchanges, blockchain analytics firms, and law enforcement is becoming central to that effort.

For everyday users, the practical takeaway is about awareness. Romance scams and “pig butchering” schemes succeed by exploiting trust and emotion, not technical vulnerabilities. No amount of blockchain security protects someone who is manipulated into sending funds voluntarily. The best defense remains skepticism toward online relationships that move toward money, unsolicited investment opportunities, and anyone who creates urgency around a crypto transfer. Thailand’s Cyber Crime Investigation Bureau alone reportedly receives around 800 crypto-related fraud complaints a day, a reminder of how relentless this threat has become.

Operation First Light took $293 million and nearly 6,000 alleged criminals out of circulation. It’s a genuine victory. But the single wallet at its center, handling $122 million in ten months, is a sobering measure of the scale that remains. The fight against crypto-enabled fraud is not close to over. What this operation proves is that coordinated, cross-border enforcement with rapid payment-freezing tools can actually land meaningful blows against it.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Cryptocurrency investments carry significant risk. Always conduct your own research before making any investment decisions.