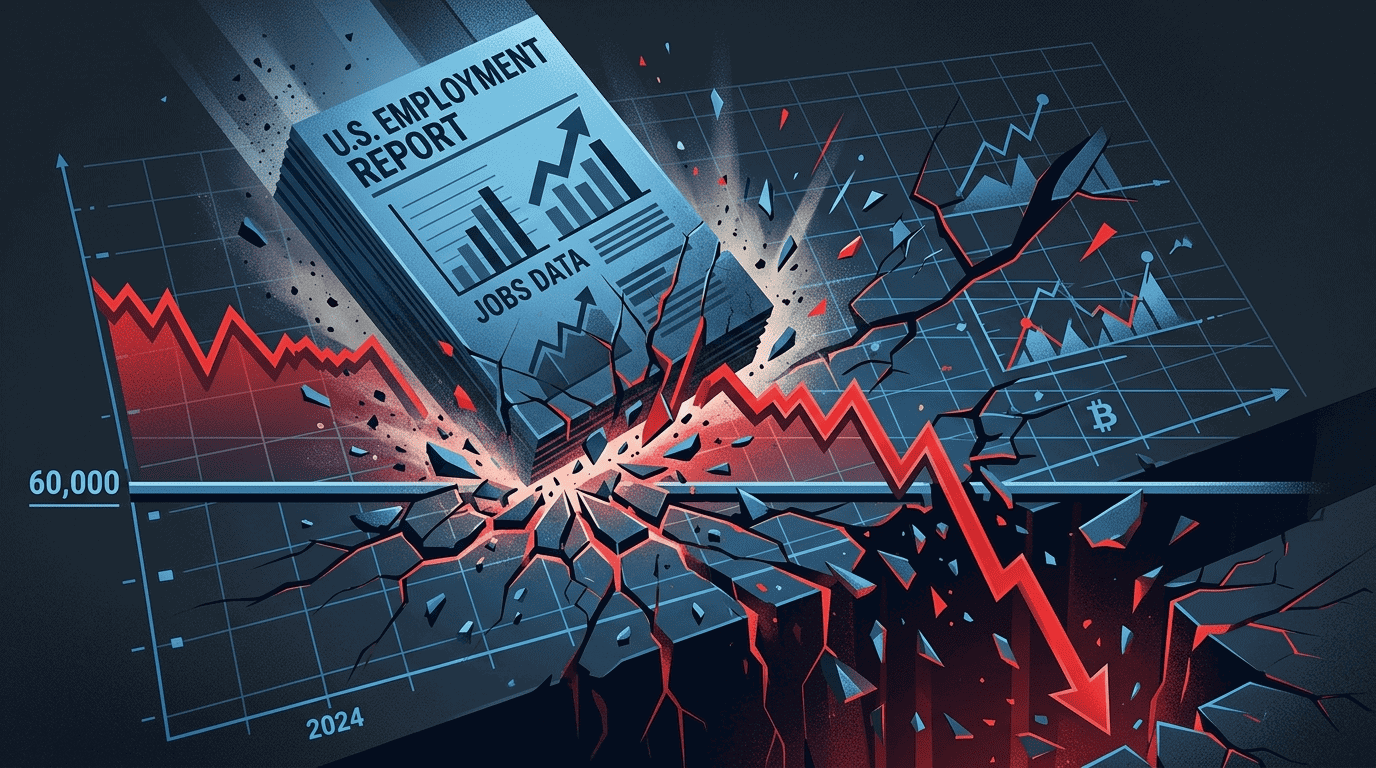

Bitcoin dropped to $59,770 on Friday afternoon. The $60,000 level that held through every crisis this year, through the Iran airstrikes, through the ETF outflow streak, through Strategy’s first sale, finally broke on a jobs report.

The US economy added 172,000 nonfarm payrolls in May, crushing expectations of 85,000. The unemployment rate held at 4.3%. April’s number was revised upward by 64,000 jobs. It was the second strongest employment report in 13 months.

For anyone hoping the economy was slowing enough for the Fed to cut rates, the data was devastating. A hot labour market means persistent inflation pressure. Persistent inflation means no rate cuts. No rate cuts means risk assets stay under pressure. And Bitcoin, which had been pricing in at least the possibility of easing, lost its last macro lifeline.

BTC is now down 20% in a single week and 52% from its October all-time high. It’s trading below the level it held when Trump won the presidency in November 2024. The crypto-friendly president, the crypto-friendly Fed Chair, the executive orders, the ARMA bill, the CLARITY Act, none of it matters when the jobs market tells the Fed that rates need to stay high or go higher.

The Rate Hike Scenario Nobody Wanted to Talk About

The jobs report didn’t just kill rate cut expectations. It revived something far worse.

BNP Paribas abandoned its forecast for stable monetary policy this week and now projects three Federal Reserve rate hikes beginning in December 2026. The bank cited persistent inflation risks, firm employment conditions, and the potential impact of the US-Iran conflict on energy prices.

Polymarket assigned a 52% probability to a Fed rate increase before year-end following the data. CME FedWatch showed a 42.7% chance that rates will be higher by December. Three months ago, the market was pricing in two to three rate cuts by year-end. Now it’s pricing in the possibility of hikes.

That shift represents a complete reversal of the macro thesis that supported Bitcoin’s rally from $60,000 to $126,000 between late 2024 and October 2025. The entire bull case rested on a premise that the Fed would ease monetary policy, making non-yielding assets like Bitcoin more attractive and pushing institutional capital down the risk spectrum.

If the Fed is tightening instead of easing, that premise collapses. Higher rates make Treasury bonds more attractive. They increase borrowing costs for leveraged crypto positions. They push institutional capital toward fixed income and away from speculative assets. And they remove the catalyst that every Bitcoin analyst has been counting on for the second half recovery.

Kevin Warsh’s first FOMC meeting is June 17-18. The jobs data gives him almost no room to signal dovishness even if he wanted to. Walking into his first rate decision with 172,000 jobs and 3.8% inflation, signalling cuts would undermine his credibility before it’s established. The market is now bracing for Warsh to hold rates steady at best and signal a hawkish bias at worst.

The Numbers That Define This Crash

The scale of destruction across Bitcoin’s holder base has reached levels not seen since the worst moments of previous bear markets.

Short-term holders, those who purchased within the last 155 days, are realising losses at the highest rate in Bitcoin’s entire history. Market analyst Scott Melker noted that the short-term holder realised profit/loss ratio hit a new all-time low, deeper than any previous drawdown including the 2022 bear market.

Long-term holders now control approximately 5.3 million BTC at a loss. That figure exceeds post-FTX levels and represents the highest amount of underwater long-term supply since the COVID-era crash in March 2020. When long-term holders are underwater in those quantities, it signals that even the strongest hands in the market are feeling pain.

Derivatives markets amplified the selling. Over $1.7 billion in leveraged positions were liquidated following the jobs report, adding to the roughly $4 billion in total liquidations over the preceding week. The Supertrend indicator on the daily chart now sits near $69,700 and acts as immediate overhead resistance, a level that failed recovery attempts have been unable to reclaim.

Presto Research analysts said Bitcoin’s decline reflects intensifying competition from gold, which hit $5,000 this year, and artificial intelligence stocks, which continue posting record earnings. The institutional money leaving Bitcoin ETFs isn’t going to cash. It’s going to Nvidia, to semiconductor funds, and to AI infrastructure plays that are delivering returns crypto can’t match right now.

Strategy’s $14 Billion Problem

Strategy’s situation has gone from bad to catastrophic in the space of five days.

The company holds 843,706 BTC at an average cost basis of $75,699. At $59,770, the entire position is approximately $13.4 billion underwater. That’s up from $5.7 billion underwater when Strategy confirmed its first Bitcoin sale on June 1, and $12.4 billion when Bitcoin was at $61,000 on Wednesday.

MSTR shares have lost over 60% from their highs. The company that turned itself into a leveraged Bitcoin holding vehicle has watched its core thesis, that Bitcoin only goes up over time and never needs to be sold, unravel in real time. The 32 BTC sold for dividends last week now looks less like inoculation and more like the first crack in a dam.

Strategy isn’t the only corporate holder in trouble. Trump Media holds Bitcoin purchased at an average of $118,522 per coin, sitting on losses exceeding $500 million. Sequans Communications is actively liquidating its 658 BTC stack. Dozens of smaller Bitcoin treasury companies that copied Strategy’s model during the bull market are now evaluating whether to continue or cut their losses.

What Breaking $60,000 Means Technically

The February 2026 low near $60,000 was the last major support level that the market respected. Bitcoin touched it, bounced, and rallied to $82,000 over the following two months. That level represented the floor of the post-halving cycle and the line between “severe correction” and “bear market.”

That line just broke. Bitcoin closed below $60,000 for the first time since October 2024. The structure of higher lows that defined the 2024-2026 bull market has been invalidated. The price is making new lows for the first time since the cycle began.

Below $60,000, technical support thins considerably. The $55,000 to $57,000 zone is the next area where meaningful buying interest exists based on historical volume profiles. Below that, $50,000 becomes the target, a level that Standard Chartered’s Geoffrey Kendrick warned about in February if ETF outflows accelerated. That scenario, which seemed extreme at the time, is now playing out.

The 200-week simple moving average, which has marked the floor of every previous Bitcoin bear market, sits near $52,000 to $54,000. If Bitcoin’s current decline follows the pattern of previous cycles, that moving average is where the selling finally exhausts itself. Getting there would represent a 57% drawdown from the all-time high, roughly in line with the kind of corrections Bitcoin has experienced in previous post-halving periods.

The Week That Changed Everything

Rewind seven days and Bitcoin was at $73,500. The market was concerned about ETF outflows and the Iran situation but still fundamentally believed that a second-half recovery was coming. Rate cuts were expected. The CLARITY Act was advancing. Warsh was going to be a friend to crypto.

In seven days: Strategy sold Bitcoin for the first time. Bitcoin crashed from $73,500 to $59,770. Over $5 billion in leveraged positions were liquidated. BNP Paribas forecast three rate hikes. Short-term holders started realising losses at the highest rate in history. The $60,000 support that held since February broke. And Bitcoin fell below the price it held when Trump won the election.

One week erased the entire thesis. Not gradually. Not with warning. In seven days.

The FOMC meeting on June 17-18 is now the most consequential date in Bitcoin’s near-term future. If Warsh somehow finds room for dovish signals despite Friday’s data, the market could stage a relief rally. If he confirms what the jobs report implies, that rates are staying high or going higher, Bitcoin’s next stop is $55,000 and the conversation shifts from “when does the recovery start” to “how deep does the bear market go.”

FAQ

Why did Bitcoin crash below $60,000?

The US economy added 172,000 jobs in May versus expectations of 85,000, crushing hopes that a weakening labour market would give the Fed room to cut rates. BNP Paribas responded by forecasting three rate hikes starting December. The data removed Bitcoin’s last macro catalyst and pushed the price from $63,000 to $59,770 on Friday, its lowest level since Trump’s election in October 2024.

Are rate hikes actually coming?

Polymarket assigns a 52% probability to at least one Fed rate increase before year-end. CME FedWatch shows a 42.7% chance. BNP Paribas forecasts three hikes starting December. The hot jobs data makes cuts nearly impossible in the near term and brings hikes into the conversation for the first time since early 2025. The FOMC meeting on June 17-18 will provide the clearest signal yet.

How much has Bitcoin fallen this week?

Bitcoin dropped approximately 20% in a single week, from $73,500 on May 31 to $59,770 on June 5. It’s now 52% below the October 2025 all-time high of $126,198. Over $5 billion in leveraged positions were liquidated during the decline. Short-term holders are realising losses at the highest rate in Bitcoin’s entire history.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments carry significant risk. Always conduct your own research before making any investment decisions.