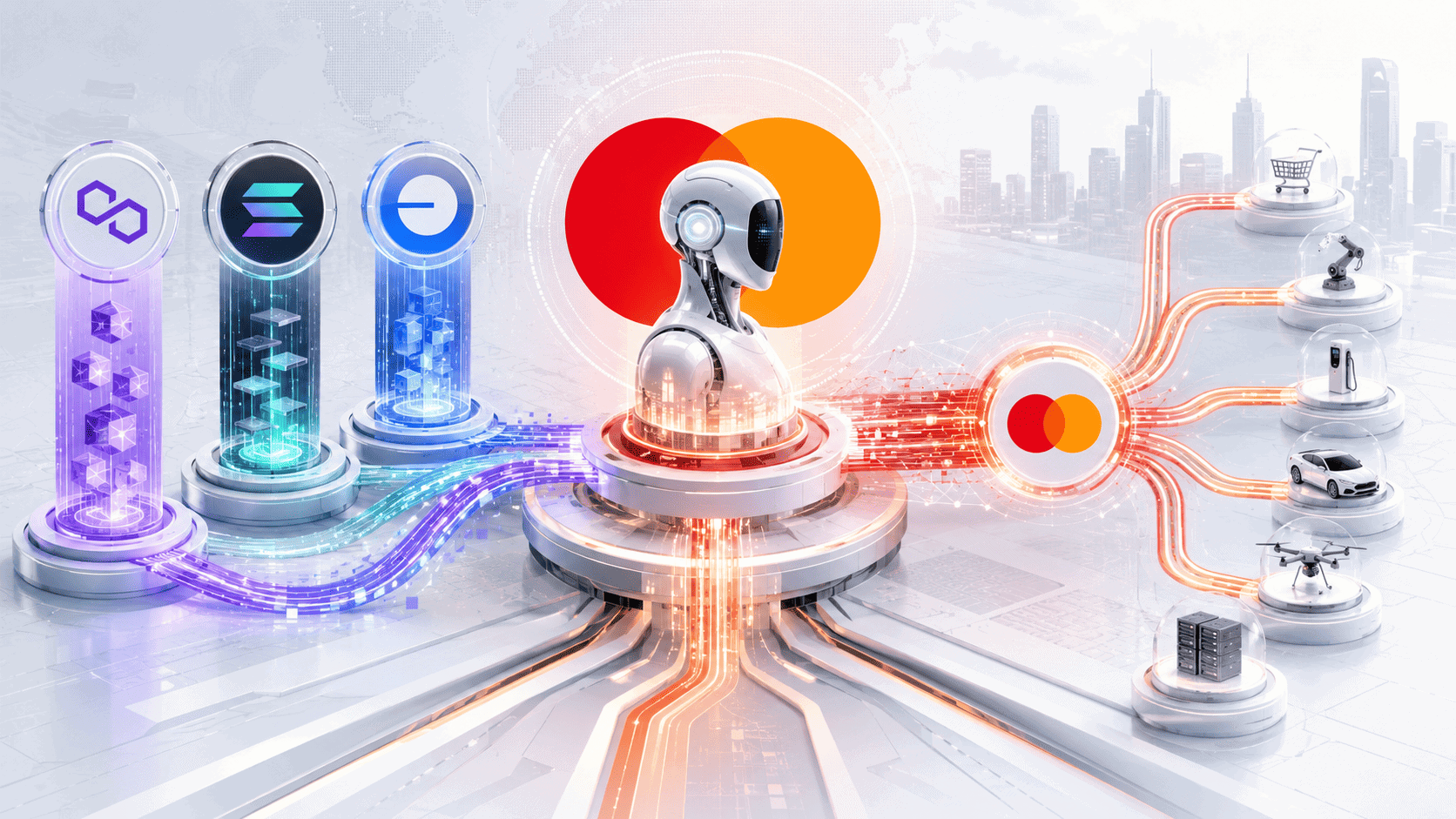

Mastercard officially launched Agent Pay for Machines (AP4M) on June 10, an open protocol enabling AI agents to authorise, coordinate, and settle transactions across the company’s global payment network at machine speed. The launch arrived with 31 named partners and a detail that the broader market is still digesting: agent permissions and credentials are stored on public blockchains, specifically Polygon, Solana, and Base.

It’s the first time a tier-one payments network has used blockchain infrastructure as the authorisation layer for its own commerce protocol. The decision isn’t symbolic. When AI agents need to verify spending permissions, they query Polygon, Solana, or Base. Public crypto networks just became the trust layer for a Mastercard product designed to facilitate machine-to-machine transactions at fractions of a cent per payment.

The partner list spans the spectrum of financial infrastructure. Traditional payment giants Stripe, Adyen, Cloudflare, Checkout.com, and Global Payments. Crypto exchanges Coinbase, OKX, and MoonPay. Layer 1 and Layer 2 blockchains Solana Foundation, Polygon, and Base. DeFi protocol Aave Labs. Custody provider Anchorage Digital. Stablecoin and on-ramp companies BVNK, Rain, Crossmint, and Utila. RippleX, the developer arm of Ripple. Thirty-plus companies that wouldn’t normally appear on the same announcement now share a single launch.

The vision Mastercard described in the announcement is significant. As AI agents begin to act on behalf of users and businesses, payments need to move into the background and operate at machine speed and massive scale. Agent Pay for Machines is the framework that makes that possible, and it’s built on rails that include both traditional finance and crypto infrastructure.

What Agent Pay for Machines Actually Does

The product solves a specific problem that’s becoming urgent as AI agents become more capable.

Imagine an AI agent acting on behalf of a business. It needs to purchase cloud computing resources from one provider, data from another, and translation services from a third. Each transaction is small, maybe fractions of a cent. The AI executes hundreds of these transactions per minute across multiple providers, each operating on different settlement systems with different identity requirements.

Traditional payment infrastructure can’t handle that volume or that velocity. Card networks are designed for human-initiated transactions with manual approval and human-scale processing. Bank transfers settle on business hours. Even instant payment systems were designed for consumer-to-merchant rather than machine-to-machine commerce.

Agent Pay for Machines provides the infrastructure layer for this new class of payments. The protocol handles three core functions. First, it verifies that an AI agent has been authorised by its human principal to spend on specific categories at specific limits. Second, it coordinates the actual settlement across multiple payment methods including cards, bank accounts, stablecoins, and digital assets. Third, it ensures that every transaction can be audited and reversed if necessary, maintaining the consumer protections that traditional payments provide.

The system supports transactions worth fractions of a cent, opening up entirely new economic models. AI agents can pay for individual API calls, single sentences of generated content, or specific data queries. The micropayment infrastructure that crypto has been promising for over a decade is now arriving through a Mastercard-led protocol with on-chain credentialing.

Why Polygon, Solana, and Base Got Chosen

The blockchain selection is the part of the announcement that matters most for the crypto industry. Mastercard could have built its credentialing system on a private blockchain controlled by the company. Instead, it chose three public networks.

The reasoning, based on the technical requirements of the system, makes sense. Each network selected has spent years developing the throughput, low transaction costs, and developer ecosystems needed to make on-chain credentialing economically viable for fractions of a cent payments.

Polygon was selected as the initial blockchain for recording human-granted permissions for AI agents. The choice reflects Polygon’s strengths in low-cost settlement and its existing institutional relationships through Polygon CDK and supernet partnerships.

Solana provides the speed needed for high-volume credential verification. The network’s sub-second finality and capability to handle thousands of transactions per second make it suitable for AI agents that need to verify permissions before executing rapid sequences of microtransactions.

Base, Coinbase’s Layer 2 network, provides Ethereum-compatible infrastructure with deep integration into Coinbase’s broader product suite. Given that Coinbase is also a launch partner providing custody services for AI agent payments, Base’s inclusion creates a tight integration loop between Coinbase’s exchange operations, custody services, and the underlying credentialing infrastructure.

The selection has implications that go far beyond Mastercard’s product. When the world’s second-largest payment network chooses three public blockchains to host the trust layer for its AI commerce framework, it validates those networks as institutional-grade infrastructure in a way that token rallies or exchange listings never could. Polygon, Solana, and Base just received the most significant institutional validation of their existence.

The Stablecoin Angle

The crypto integration extends beyond credentialing. Stablecoin settlement is built into Agent Pay for Machines as a core feature.

Mastercard’s parallel stablecoin settlement initiative covers multiple blockchain networks including Ethereum, Solana, Polygon, Base, Arbitrum, Canton, Tempo, and the XRP Ledger. AI agents using AP4M can settle transactions in stablecoins on any of these networks, with Mastercard providing the bridge to traditional banking infrastructure when needed.

The first phase of stablecoin settlement covers parts of the United States and Latin America, with expansion planned through the rest of 2026. The geographic rollout reflects regulatory clarity in those markets. The US has the GENIUS Act for stablecoins. Latin American markets have growing crypto adoption and limited regulatory barriers to stablecoin settlement.

For RippleX, the XRP Ledger’s inclusion is a significant validation. The settlement service operates on XRPL alongside Ethereum, Solana, and the other supported networks. That positions XRP and the XRP Ledger as one of the eight blockchains Mastercard considers suitable for institutional-grade stablecoin settlement.

The broader implication is that AI agents won’t be confined to a single payment rail. They can settle in USDC on Solana for a content provider, in stablecoin via the XRP Ledger for an international vendor, or via traditional Mastercard rails for a card-accepting merchant. The choice of settlement method becomes a parameter the AI agent optimises based on speed, cost, and counterparty preference rather than a hard infrastructure constraint.

What This Means for the Crypto Industry

The launch represents one of the most significant institutional crypto integrations of 2026, though it might not be priced into token valuations yet.

For Polygon, Solana, and Base, the AP4M selection creates a structural new use case that goes beyond DeFi, NFTs, or gaming. AI agent credentialing is potentially one of the largest categories of blockchain transactions over the next decade. As AI deployment expands across businesses, the volume of credentialing transactions could exceed many other categories combined.

For Aave Labs, the inclusion as a launch partner reinforces the protocol’s positioning as financial infrastructure rather than just a DeFi lending app. Aave founder Stani Kulechov noted that machine payments require both payments infrastructure and treasury management capabilities, suggesting Aave could provide credit and liquidity to AI agents that need to manage cash flows across transactions.

For RippleX, the XRP Ledger’s inclusion in Mastercard’s settlement layer validates Ripple’s long-standing thesis that XRPL is institutional payment infrastructure. The token price doesn’t reflect this validation yet, but the structural significance is significant.

For Coinbase, providing custody for AI agent payments alongside Base’s role in credentialing creates a vertically integrated stack that no other crypto firm can match. Coinbase processes the agent’s payments, holds the agent’s funds, and the credentials live on Coinbase’s blockchain. That integration is exactly what large enterprises deploying AI agents will want.

The broader pattern continues. SoFi launched a bank-issued stablecoin. JPMorgan settled on the XRP Ledger. Japan’s three megabanks are launching a yen stablecoin. DTCC connected to Stellar. And now Mastercard built AI payment infrastructure on three public blockchains. The institutional integration of crypto isn’t theoretical anymore. It’s the dominant story of 2026, hidden in plain sight beneath the price action.

FAQ

What is Mastercard’s Agent Pay for Machines?

AP4M is an open protocol enabling AI agents to authorise, coordinate, and settle transactions across Mastercard’s global payment network at machine speed. The system supports transactions worth fractions of a cent and operates with 31 launch partners including Coinbase, Ripple, Polygon, Solana, and Aave Labs. Agent permissions are stored on public blockchains.

Which blockchains are involved?

Agent permissions and credentials are stored on Polygon, Solana, and Base. Stablecoin settlement operates across a broader set including Ethereum, Solana, Polygon, Base, Arbitrum, Canton, Tempo, and the XRP Ledger. Polygon was selected as the initial blockchain for recording human-granted permissions for AI agents.

Why does this matter for crypto?

For the first time, a tier-one payments network has used public blockchain infrastructure as the authorisation layer for its own commerce protocol. Polygon, Solana, and Base receiving this institutional validation positions them as foundational infrastructure for AI commerce, potentially one of the largest categories of blockchain transactions over the next decade. The selection represents a significant institutional adoption milestone that goes beyond ETF flows or token speculation.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments carry significant risk. Always conduct your own research before making any investment decisions.