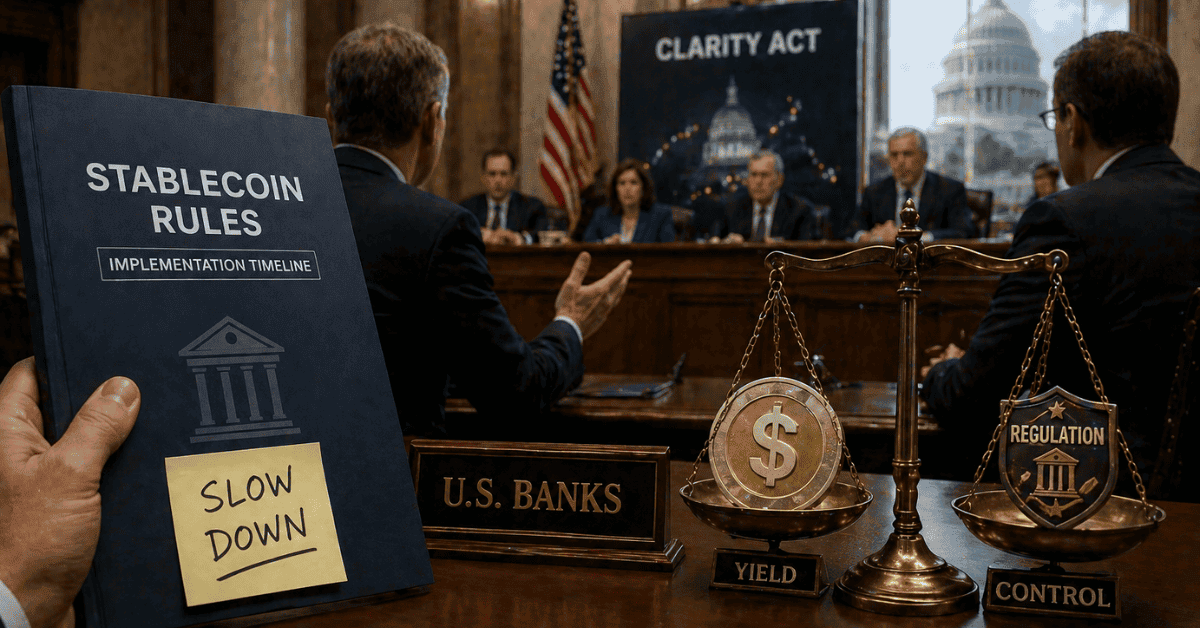

US banks are pushing to slow and reshape new stablecoin rules, with the biggest fight centered on one question: should stablecoin users be able to earn yield?

The banking industry is pressing regulators for more time before key GENIUS Act rules take effect, while also lobbying lawmakers to tighten language in the CLARITY Act. The goal is to limit or block stablecoin rewards that could make tokenized dollars more attractive than ordinary bank deposits.

The dispute matters because stablecoins are no longer just crypto trading tools. They are becoming digital versions of cash, backed by dollars, Treasury bills and other short-term assets. If they can also offer attractive yields through exchanges or affiliated platforms, banks worry they could compete directly with savings accounts and money market products.

That makes the stablecoin debate one of the most important regulatory fights in Washington.

The GENIUS Act Set the First Rules, But Banks Want More Time

The GENIUS Act, signed into law in July 2025, created a federal framework for payment stablecoins. It requires stablecoin issuers to back tokens one-to-one with approved reserve assets, including cash, bank deposits, short-term Treasuries and certain money market funds.

The law also prohibits stablecoin issuers from directly paying interest or yield to holders. But it does not fully close the door on rewards offered by affiliates, crypto exchanges or other third-party platforms.

That gap is now the battleground.

CryptoSlate reported that major banking associations are seeking a 60-day extension on comment periods tied to GENIUS Act rulemaking. The practical effect would be to slow the rollout of regulated nonbank stablecoin infrastructure, giving banks more time to influence the final rules.

For banks, the concern is not only compliance. It is competition.

Why Yield Is the Core Fight

The banking industry’s worry is straightforward. If stablecoin platforms can pass on Treasury yield to users, stablecoin accounts could become more attractive than low-yield bank deposits.

That matters because deposits are the foundation of traditional banking. Banks use deposits to fund loans, manage liquidity and support their broader business model. If consumers or businesses move meaningful amounts of cash into stablecoins, banks argue that credit availability could be affected.

Reuters reported earlier this year that a White House meeting between major banks and crypto firms failed to resolve the disagreement. The key sticking point was stablecoin rewards, with banks pushing to prohibit them and crypto companies arguing that rewards are important for customer acquisition and competition.

The White House Council of Economic Advisers has also described the issue directly. Its April 2026 analysis said the GENIUS Act bans issuers from paying interest, but does not explicitly prohibit affiliate or third-party arrangements that might offer interest-bearing products. Some versions of the CLARITY Act would close that channel.

That is why the fight has moved from stablecoin issuance to stablecoin economics.

CLARITY Act Has Become the Main Battleground

The Digital Asset Market Clarity Act, known as the CLARITY Act, is supposed to create a broader federal framework for digital assets. It would clarify how crypto tokens are regulated, define the roles of the SEC and CFTC and create a path for certain digital assets to be treated as non-securities once their networks mature.

But stablecoin yield has become one of the biggest obstacles to progress.

Galaxy Research said the CLARITY Act passed the House in July 2025 with strong bipartisan support, 294 to 134, but has been tied up in Senate negotiations since January. The report said three key issues remained unresolved in late April: stablecoin yield language, DeFi provisions and securing enough Republican votes on the Senate Banking Committee.

That timing is important. The Senate calendar is crowded, and delays matter. Galaxy said a markup slipping past mid-May could sharply reduce the chances of the bill becoming law in 2026.

Crypto firms want the bill to move because regulatory clarity could bring more institutional capital into the sector. Banks want the bill shaped in a way that stops stablecoins from becoming deposit-like products with yield.

What Banks Are Really Protecting

At the surface, this is a technical legal debate about who can pay yield and under what structure.

Underneath, it is a fight over who controls digital dollars.

If stablecoins are limited to payments only, banks can live with them more easily. They become faster settlement tools, useful for crypto trading and some payment flows, but less threatening to bank deposits.

If stablecoins can offer yield through exchanges or partner platforms, they become something more powerful. They start to look like digital cash accounts that can compete with banks for customer balances.

That is why banking groups are focused on closing the third-party rewards channel. The GENIUS Act already stops issuers from paying interest directly. Banks now want to make sure crypto platforms cannot recreate the same outcome through rewards, incentives or affiliate products.

For the crypto industry, that would remove one of the clearest consumer benefits of holding stablecoins instead of dollars in a bank account.

The May Markup Could Decide the Path Forward

The next major catalyst is a potential May markup of the CLARITY Act in the Senate Banking Committee.

A markup would allow senators to debate, amend and vote on the bill before it moves further through the legislative process. If lawmakers reach a compromise on stablecoin yield, the broader market structure bill could regain momentum.

If they do not, the issue could remain stuck for months or even years.

That uncertainty matters for stablecoin issuers, exchanges, banks and investors. A clear rulebook could accelerate adoption of regulated dollar stablecoins in the US. A prolonged delay could push more activity offshore, where stablecoin products may face different standards.

It could also affect how companies design future stablecoin products. A yield ban would favor payment-focused stablecoins. A more flexible framework could support rewards, savings-like products and deeper integration with crypto exchanges.

The Bottom Line

US banks are not trying to stop stablecoins entirely. They are trying to make sure stablecoins do not become high-yield competitors to bank deposits.

That is why they are pushing for more time on GENIUS Act implementation and tighter language in the CLARITY Act. The fight is no longer only about whether stablecoins should be legal. It is about how attractive they are allowed to become.

For crypto, the outcome could shape the next phase of dollar stablecoin growth. For banks, it could determine how much deposit competition they face from tokenized cash.

The May CLARITY Act markup may show whether Washington can find a compromise. Until then, the future of stablecoin yield in the US remains one of the biggest unresolved questions in crypto regulation.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice. Always conduct your own research before making any investment decisions.