For decades, one company has controlled how every stock trade in America gets finalized. The Depository Trust and Clearing Corporation, better known as the DTCC, has been the invisible plumbing behind virtually every equity transaction in the United States since the 1970s.

That monopoly just got its first real challenger.

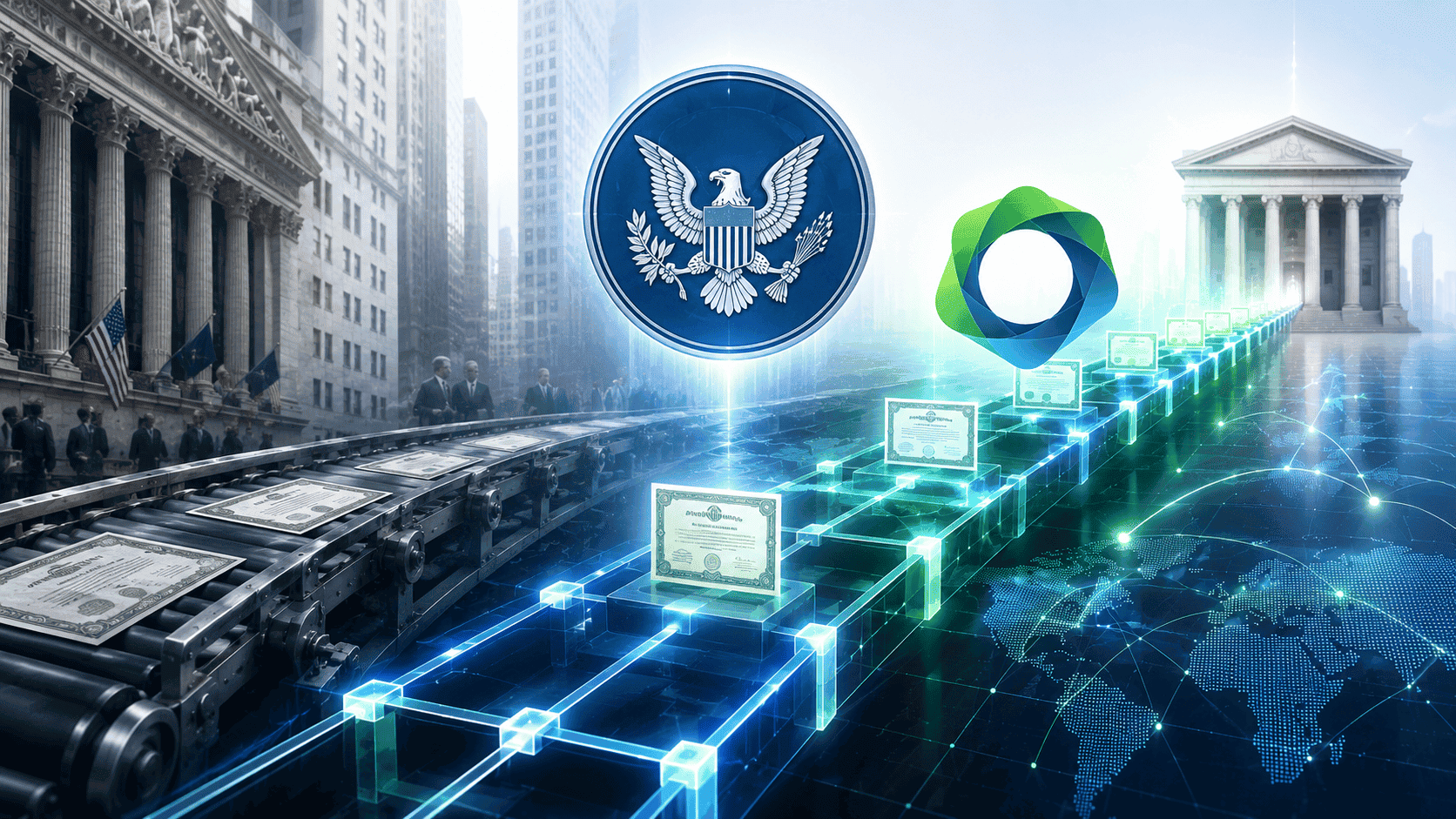

The SEC granted Paxos Securities Settlement Company full registration as a clearing agency under Section 17A of the Securities Exchange Act of 1934 on Thursday. The approval makes Paxos the first and only blockchain-native firm authorized to operate as a central securities depository in the United States.

In practical terms, Paxos can now clear and settle eligible US stock trades on blockchain rails, delivering same-day settlement that eliminates the waiting period built into the traditional system. Seven years of regulatory engagement, starting with a 2019 no-action letter and a 2020 pilot that processed real equity trades for AT&T and General Electric, have culminated in a moment that could reshape how trillions of dollars in securities change hands.

CEO and co-founder Charles Cascarilla called it the result of “seven years of work with the SEC.” Those seven years just paid off.

Why Settlement Speed Matters More Than You Think

To understand why this approval is so significant, you need to understand what happens after you click “buy” on a stock.

When you purchase shares of Apple or Tesla through your brokerage, the trade executes in milliseconds. But the actual exchange of money for legal ownership of those shares doesn’t happen instantly. It goes through a settlement process managed by the DTCC that currently takes one full business day. That’s called T+1 settlement, and it only became the standard in 2024 after decades of T+2 (two-day) settlement.

During that settlement window, capital is effectively locked. The buyer’s money and the seller’s shares are both in limbo, committed but not yet exchanged. For institutional investors managing billions of dollars across thousands of daily trades, that locked capital represents an enormous opportunity cost. Money sitting in a settlement can’t be invested, lent, or deployed elsewhere.

Paxos eliminates that window entirely. Its blockchain-based system delivers what’s called T+0 settlement, meaning the exchange of money for shares happens on the same day the trade executes. In many cases, it can settle in minutes rather than hours.

For a single retail investor buying 10 shares of a stock, the difference between T+1 and T+0 is irrelevant. For a hedge fund executing $500 million in trades per day, instant settlement frees up hundreds of millions in capital that would otherwise be trapped in the clearing process. Multiply that across Wall Street and the efficiency gains run into the billions.

How the DTCC’s Monopoly Worked

The DTCC has been one of the most important and least understood institutions in American finance. It processes roughly $2.5 quadrillion in securities transactions annually. Virtually every stock, bond, and derivative trade in the United States passes through its systems.

That dominance wasn’t accidental. After the paperwork crisis of the late 1960s, when Wall Street literally couldn’t process the volume of physical stock certificates being traded, Congress authorized the creation of centralized depositories to manage the post-trade process electronically. The DTCC emerged from that mandate and has held its position ever since.

The system works. It’s reliable and well-regulated, and it has processed trillions of transactions without a systemic failure. But it’s also slow by modern standards, expensive to maintain, and built on infrastructure that predates the internet.

Paxos isn’t trying to replace the DTCC overnight. The SEC registration is described as temporary, and Paxos will initially handle a limited set of eligible securities. But the precedent matters enormously. A blockchain-native company now operates under the same regulatory framework as the DTCC. It’s authorized to perform the same functions. And it can do them faster.

The DTCC itself isn’t standing still. It announced plans to launch its own tokenization service in October 2026 with input from over 50 firms, including Goldman Sachs and Circle. The legacy institution recognizes the threat and is adapting. But adapting from the inside is different from being disrupted from the outside, and Paxos is firmly on the outside.

What Paxos Has Already Proven

This approval didn’t come from a theoretical proposal. Paxos has been running real settlements on blockchain for years.

The 2019 SEC no-action letter allowed Paxos to conduct a controlled pilot with a small number of broker-dealers. The pilot processed actual equity trades for companies including AT&T and General Electric, settling them on blockchain infrastructure while maintaining full regulatory compliance.

That pilot ran for nearly six years, generating detailed performance data that the SEC used to evaluate Paxos’s full clearing agency application. The data showed that blockchain settlement could match or exceed the reliability of traditional systems while delivering significantly faster completion times.

Seven participants took part in the pilot. The results were consistent enough for the SEC to move from “we’ll let you try this in a sandbox” to “you’re now a registered clearing agency.” That progression from experiment to approval took seven years. It also represents one of the most thorough regulatory evaluations of blockchain technology ever conducted by a US federal agency.

Paxos has credibility beyond the settlement pilot, too. The company issues PayPal’s PYUSD stablecoin, one of the largest stablecoins in circulation. It holds an OCC-approved national trust charter. And it operates a regulated blockchain infrastructure for institutional clients across multiple product lines.

What This Means for Tokenised Securities

The Paxos approval lands at a moment when the entire financial industry is debating how quickly to bring securities onto blockchain.

The SEC delayed its tokenised stock exemption earlier this week after concerns about third-party tokens disrupting corporate governance. That delay slowed one path to on-chain equities. Paxos’s clearing agency registration opens a different, potentially more powerful path.

Rather than tokenising stocks as new digital assets that trade on crypto platforms, Paxos can settle traditional stock trades using blockchain as the backend infrastructure. The stocks themselves don’t need to change. The exchanges don’t need to change. The brokerages don’t need to change. Only the settlement layer changes, from DTCC’s legacy system to Paxos’s blockchain rails.

That approach is less disruptive and more likely to gain rapid institutional adoption because it doesn’t require anyone in the existing financial ecosystem to fundamentally alter how they operate. Brokers still send orders to exchanges. Exchanges still match buyers and sellers. The only difference is that the final step, the actual exchange of money for ownership, happens faster and on a different type of infrastructure.

For the tokenization movement broadly, Paxos’s approval validates the thesis that blockchain can handle the most critical, heavily regulated functions in financial markets. If the SEC trusts blockchain enough to register a clearing agency, the argument that blockchain isn’t ready for institutional finance loses most of its weight.

The Seven-Year Lesson for the Crypto Industry

There’s a broader lesson in Paxos’s story that the crypto industry should heed.

Seven years. That’s how long it took from the first SEC engagement in 2019 to full clearing agency registration in 2026. Seven years of pilots, data collection, regulatory dialogue, compliance buildout, and incremental progress.

In an industry that measures time in token launch cycles and quarterly price movements, seven years of patient regulatory work is almost unheard of. Most crypto companies want approval next quarter. Paxos spent the better part of a decade earning it.

The result is an approval that no competitor can easily replicate. The regulatory moat around Paxos’s clearing agency registration is enormous. Any challenger would need to go through a similarly extended engagement with the SEC, conduct multi-year pilots, demonstrate consistent reliability, and meet the same compliance standards that Paxos spent seven years building.

For an industry that often prioritizes speed over substance, Paxos’s story is a reminder that the most valuable positions in regulated finance are built slowly. And once built, they’re very hard to take away.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments carry significant risk. Always conduct your own research before making any investment decisions.